When people think about money problems in relationships, they usually picture dramatic scenarios: massive secret debt, reckless gambling, discovered hidden accounts. These things do happen and they do cause serious damage. But many relationships quietly break down over a far less dramatic financial mistake — one that’s subtle enough to go unnoticed for years, and damaging enough that by the time couples recognize it, significant harm has already been done.

That mistake is financial avoidance: the sustained pattern of not talking about money — not making decisions together, not sharing the full picture, not aligning on values or goals — in a relationship where finances are supposed to be shared.

It doesn’t feel like a mistake. It often feels like keeping the peace.

What Financial Avoidance Actually Looks Like

Financial avoidance in a relationship doesn’t always look like neglect or irresponsibility. It often looks like reasonable behavior on the surface.

It looks like the couple that has merged bank accounts but never explicitly talked about a budget — who spend more or less in alignment for a few years until a major expense reveals they have completely different ideas about how money should be managed.

It looks like the partner who pays all the bills and “doesn’t want to stress” the other person with the details — until the stress of managing everything alone becomes resentment, and the uninformed partner realizes they’ve been kept out of their own financial life.

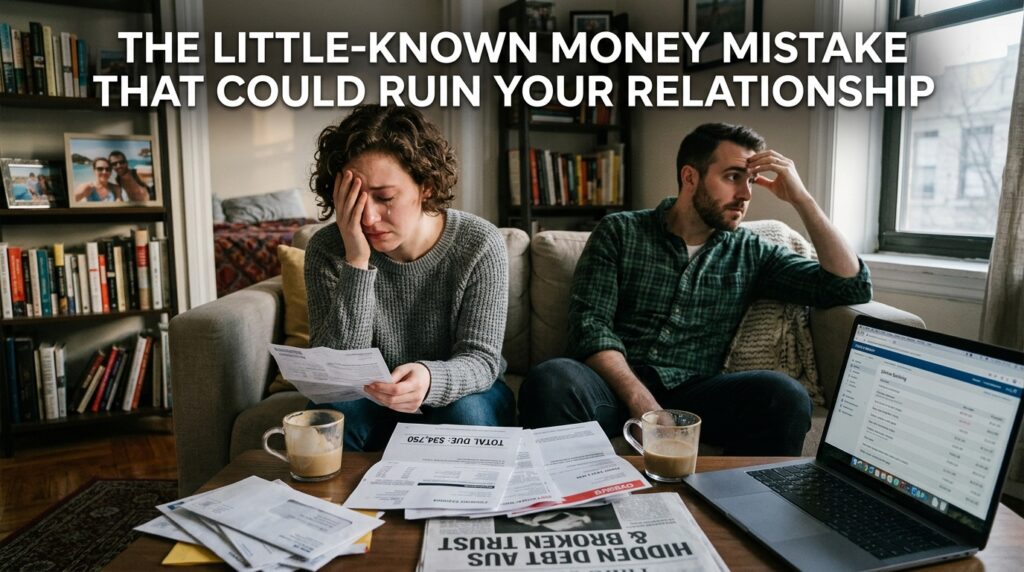

It looks like the couple who both know they have credit card debt but don’t talk about how much, because bringing it up would start a fight. So the debt grows. So does the tension.

It looks like the pair who avoid talking about retirement savings because they’re not old enough for it to feel urgent — until suddenly they’re ten years behind where they should be and arguing about how that happened.

In every case, the pattern is the same: financial reality exists, but no one is directly engaging with it together. And in that silence, small problems compound.

Why Couples Fall Into Financial Avoidance

Understanding why couples avoid financial conversations is key to breaking the pattern. The most common reasons include:

Money carries emotional weight. For many people, money is deeply connected to feelings of shame, fear, inadequacy, or identity. Discussing it with a partner feels exposing. If you carry debt or have made financial mistakes, admitting this can feel humiliating — even to someone you love.

Conflict feels worse than uncertainty. If past money conversations have ended in arguments, couples learn to avoid them. The short-term peace of not talking about it seems preferable to the stress of discussing it. This is a classic example of short-term comfort creating long-term damage.

One partner defers to the other. In relationships where one partner has more financial knowledge, confidence, or income, the other may habitually defer. Over time this creates an unhealthy dynamic where one person is disengaged from a major domain of their shared life.

Cultural and gender norms. In many cultural and family contexts, money is treated as a private subject — not discussed openly, especially between partners. These norms can be difficult to override even when you intellectually know better.

Fear of judgment. People often worry that revealing their financial habits — especially if those habits aren’t ideal — will cause their partner to think less of them. This fear of judgment keeps real conversations from happening.

How Financial Avoidance Damages Relationships Over Time

The damage is rarely sudden. That’s what makes it so difficult to catch.

In the short term, avoiding financial conversations keeps things stable. But underneath the surface, several damaging processes are at work:

Hidden stress accumulates. If one partner is managing financial anxiety alone — knowing about problems the other doesn’t — they’re carrying an invisible weight. Over time this creates emotional distance. The managing partner may begin to feel unsupported. The uninformed partner may sense that something is wrong but can’t access it because it’s never discussed.

Resentment grows. If one partner is more financially responsible than the other — saving, tracking spending, making careful decisions — and the other partner is spending freely without accountability, the responsible partner starts to feel penalized for their discipline. This is a significant and common source of long-term resentment.

Trust erodes. When financial truths eventually surface — as they tend to — the manner of their surfacing matters enormously. If your partner discovers financial information you’ve been avoiding sharing, the issue is no longer just the information. It’s also the avoidance. “Why didn’t you tell me?” is often a harder conversation than the original financial problem would have been.

Opportunities are missed. Couples who don’t discuss money miss the chance to align on goals, make proactive decisions, and build financial security together. Every year of financial avoidance is a year of potential wealth-building that didn’t happen because no one was steering.

The Financial Conversation Most Couples Never Have

Most couples have never had what financial therapists describe as a “full financial disclosure” conversation. This doesn’t mean interrogating your partner like they’re a suspect — it means sitting down together, with openness and without judgment, to share the complete picture of where you each stand financially.

This conversation covers:

- Current income from all sources

- All existing debts (credit cards, student loans, car loans, personal loans, any other obligations)

- Current savings and investments

- Monthly expenses, including ones the other partner may not be aware of

- Credit score and credit history

- Financial goals — short-term (this year), medium-term (next five years), and long-term (retirement)

- Financial fears and anxieties — what keeps each of you up at night financially

- Spending habits and tendencies (saver vs. spender, impulsive vs. deliberate)

Couples who have this conversation report that even when the information is uncomfortable, the experience of sharing it openly shifts the dynamic. It creates a foundation of honesty that makes future financial discussions less fraught.

The Role of Financial Therapy

Many people are unaware that financial therapy is a specialty field — practitioners who are trained in both financial planning and psychotherapy, and who work specifically with the emotional dimensions of money in relationships.

Financial therapists are particularly skilled at helping couples uncover the “money scripts” — beliefs about money inherited from family and culture — that are shaping their financial behavior in ways they don’t fully recognize. Common money scripts include: “Talking about money is rude,” “Rich people are greedy,” “You should always have a safety net,” “Money is for enjoying life, not hoarding it.”

These scripts, operating below the surface, drive real financial behavior and real relationship conflict. Making them explicit is often the first step to navigating them.

If financial conversations in your relationship consistently escalate into arguments or shut down entirely, working with a financial therapist — even for a few sessions — can break the logjam in ways that self-help strategies often can’t.

Practical Steps to Break the Avoidance Pattern

You don’t need to overhaul everything at once. Here are concrete steps to begin addressing financial avoidance:

Schedule a low-stakes money date. Choose a calm, relaxed time — not a stressful moment — to begin a financial conversation. Keep it short and focused: one topic at a time. This takes the pressure off and makes it a habit rather than an emergency.

Start with values before numbers. Before diving into spreadsheets, talk about what money means to each of you. What do you most want to save for? What brings you joy to spend on? What financial situation would make you feel truly secure? Starting with values creates alignment before the specific numbers, which are easier to navigate once you understand each other’s “why.”

Use a neutral third party if needed. If conversations about money reliably escalate, a financial advisor, couples therapist, or financial therapist can facilitate the conversation in a way that keeps it productive.

Create a regular check-in. Monthly or quarterly financial meetings — even brief ones — prevent the long stretches of financial silence that allow small problems to compound. Review income, expenses, progress toward goals, and any upcoming decisions. The regularity matters more than the duration.

Couples who face their financial reality together — honestly, regularly, and with mutual respect — don’t just build better finances. They build a stronger relationship. The experience of navigating something real and difficult together, without resentment or secrecy, creates a particular kind of trust and partnership that is hard to build any other way.

The money mistake that ruins most relationships isn’t dramatic. It’s the quiet daily choice to avoid the conversation one more time. The good news is that it’s entirely reversible — if you’re willing to start talking.